Unitree's IPO

robotics diffusion, AGI for the real world, and US-China entanglement

In 2017, Hangzhou-based robotics firm Unitree 宇树科技 launched its first quadruped, Laikago. Laika was the name of the Soviet space dog onboard Sputnik 2, and the American English pronunciation of “go” is similar to that of the Chinese word for dogs, 狗 gǒu. Unitree’s battery-powered tribute to Laika wasn’t fuzzy, but walked on four feet and navigated through basic obstacles.

Unitree founder Wang Xingxing 王兴兴 has long held faith in the potential of robotic canines. Since 2020, when Unitree started gaining media attention, he has insisted in multiple interviews that humans are drawn to four-legged creatures and will have a natural fondness for their artificial counterparts.

Fast forward to 2026, and Unitree has just filed for a $610-million IPO on the Shanghai Stock Exchange. The company is a household name in China after its humanoid robots performed dances at the CCTV Spring Festival Gala for two consecutive years and counting. Through their IPO disclosures (investor prospectus and response letter to the Shanghai Stock Exchange’s inquiries), we get some answers to important questions about the development of embodied AI.

How is Unitree profitable?

Where is diffusion happening inside China, aside from dancing on TV?

Are Chinese robotics companies content to lead in hardware and applications, or do they also see themselves as pursuing some kind of generalized “frontier”?

And finally, what does this all mean for US-China dynamics in robotics?

What’s the money maker?

One of the most notable things about Unitree is the fact that it actually makes money. Unprofitability is a near-universal challenge because AI robotics, despite massive advances in the past few years, is still an early-stage technology. Mass adoption has not yet arrived; pathways out of bottlenecks like data are uncertain; and important safety standards have not caught up. Even shipping products consistently can be a challenge for some companies in the space, let alone manufacturing at scale and booking reliable customers.

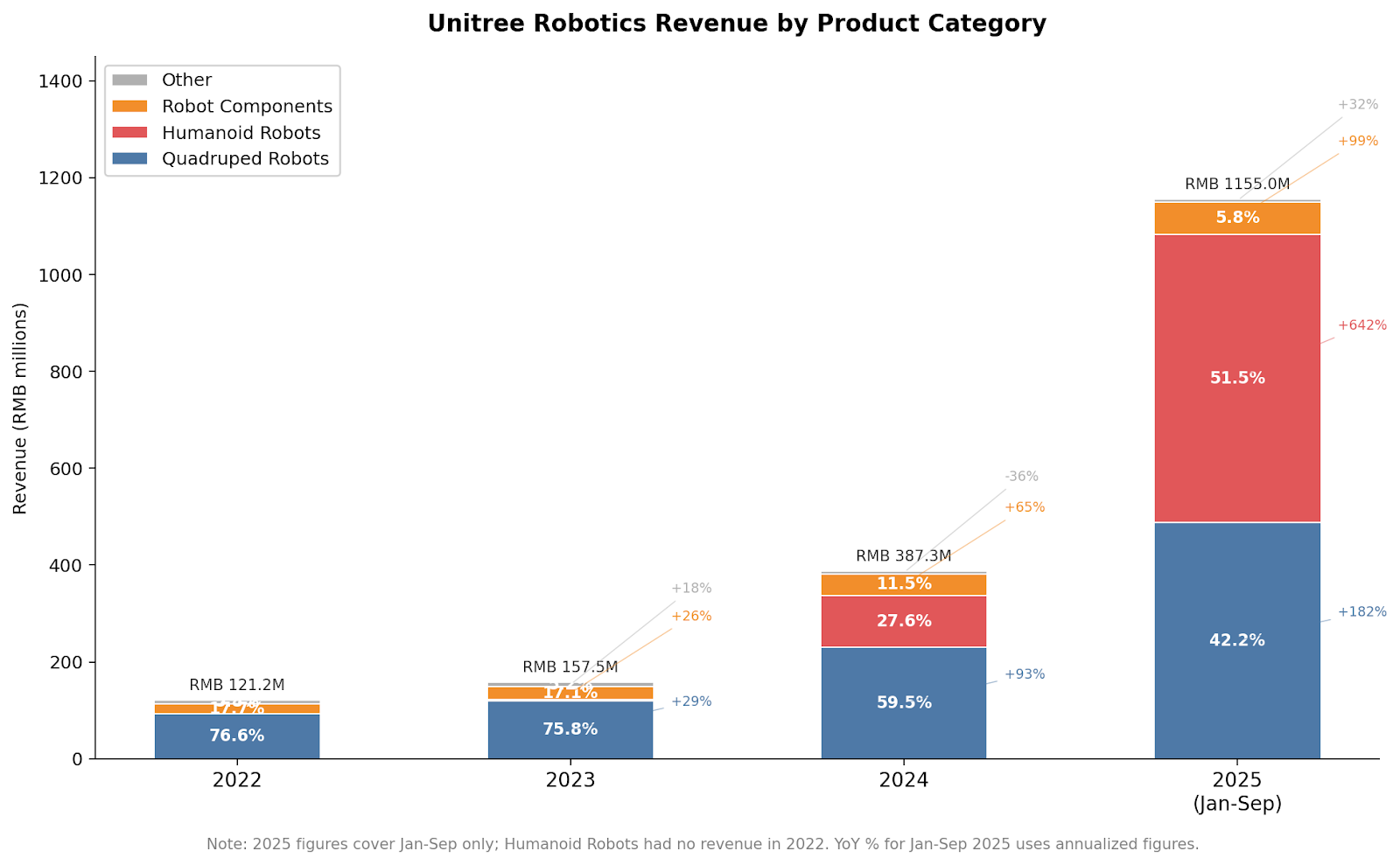

This context is why observers have found Unitree’s ability to turn a profit remarkable. Not only has the company’s net profit been positive since 2024, but from 2024 to 2025, its net profit grew by 204.29%. A look at its growth, broken down by product category, reveals the most significant source of this revenue explosion: humanoids.

It’s perhaps ironic that, despite the company’s longstanding work in quadrupeds, it is humanoids that have catapulted its business model to success. By meeting genuine demand in academia — and staging an especially strong marketing campaign in front of the Chinese public — Unitree has transformed itself into a humanoid frontrunner. Some analyses trace their potent commercialization drive back to Unitree’s origins. Wang Xingxing’s cofounder Chen Li 陈立, who was Wang’s classmate throughout both their undergraduate and Master’s programs, worked in international sales for the Hangzhou-based, partly state-owned surveillance tech giant Hikvision (海康威视) before joining Unitree. Hikvision has been extremely successful at expanding internationally (including in the US before it was added to the Entity List over its involvement in human rights abuses against ethnic and religious minorities in China). Investors have told Chinese media that Chen’s experience is an important asset for Unitree’s global commercialization, driving sales to governments and businesses in particular.

Unitree has earned name recognition in the West, but it is far from the only Chinese robotics company meaningfully shaping the future of embodied AI. In fact, it is part of an increasingly competitive market for AI-powered robots. Among listed peers, UBTECH and Dobot are major competitors named in Unitree’s prospectus. A fellow member of the “Hangzhou Six Dragons,” DEEP Robotics, is betting big on scenario-adapted applications, while AgiBot, by some estimates, shipped even more humanoid units last year than Unitree did.

In their response to the Shanghai Stock Exchange’s inquiry letter, Unitree emphasized in-house development of hardware parts as its key strategy for cutting costs. Unitree designs, builds, and assembles most components (other than commodity components like battery cells, flash storage, and the core computing board) in-house. It does offer outsourced alternatives for add-ons like LiDAR, cameras, and dextrous hands, but has also developed in-house options for all of these.

Where are the robots?

Unitree’s most reliable customers are universities, research institutions, and other companies conducting research into robotics. Its hold on academic customers worldwide is so firm that it’s caused alarm among DC policymakers. In May 2025, the China Select Committee called for Unitree to be designated as a “Chinese military company” and to be added to the Entity List.

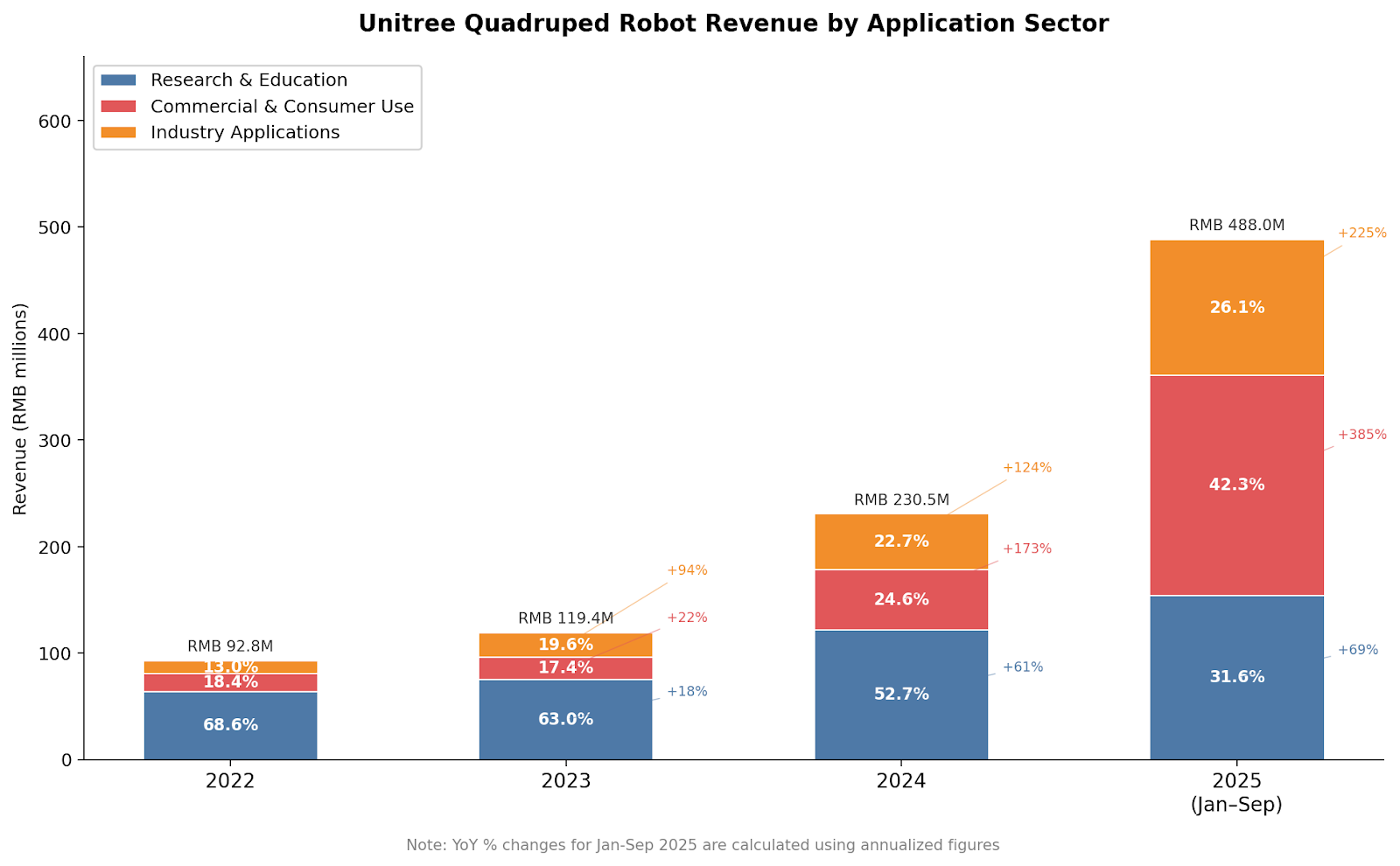

The data Unitree disclosed about its revenue sources, however, paints a more complex picture. For quadrupeds, the research and education sector has been the company’s most reliable source of revenue since at least 2022 (IPOs generally do not require companies to disclose audited financial statements from more than three years ago). But starting in 2024, revenue from both commercial and industry customers more than doubled. Consumer sales revenue nearly quadrupled year-on-year in only the first nine months of 2025.

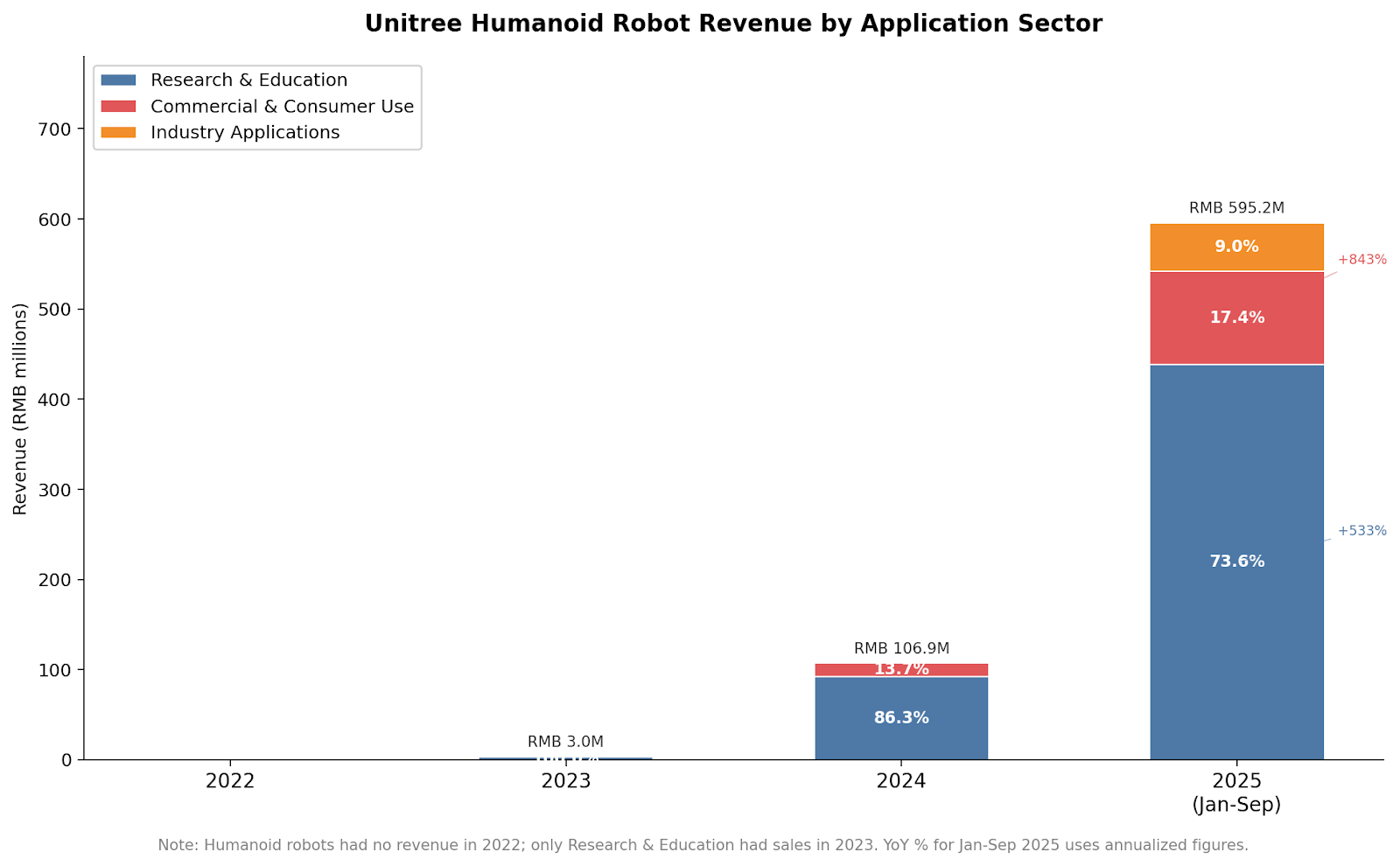

A similar, if more compact, story emerges for humanoids as well. Demand still largely comes from researchers and educational institutions, but commercial and industrial demand has grown from a near-zero starting point on a seemingly exponential trajectory since 2024. Consumers are especially excited about humanoids due to Unitree’s successful marketing of the concept. Industrial applications of humanoids are more limited compared to those of quadrupeds, but are also appearing.

What, exactly, are people doing with these robots? “Research & Education” encompasses sales to researchers, who use Unitree hardware and platforms to conduct their own experiments. The “Commercial & Consumer Use” and “Industry Applications” categories roughly map onto B2C and B2B sales, respectively. According to Unitree, non-academic consumers who buy their robots mostly do so “for show”: they’re deploying these robots as attractive promoters in retail settings, at tourist sites, and in performances and exhibitions. Some use them as novelty companions.

Applications in industry are more interesting. Quadrupeds are deployed as “smart inspectors” in power grids, subway tunnels, and gas pipelines. They can also assist in harsh settings like emergency response and outdoor surveys, and complete manufacturing and logistical tasks. E-commerce firm JD.com is Unitree’s biggest corporate customer. Humanoids, according to Unitree, are being used for inspections and manufacturing as well, though in a more limited capacity because the technology is less mature. Unitree expects consumer demand for humanoids to grow in the medium term, but we will have to wait a while longer for genuinely useful humanoids on the factory floor.

Is Unitree… AGI-Pilled?

Received wisdom in robotics has it that the US leads in software-related research, while China’s strength is in hardware. The implication is that the US is likely to reach “generalized” machine intelligence in the physical world faster than China, but — in the meantime — Chinese companies could get to practical applications faster through quick iterations inside an unparalleled manufacturing ecosystem.

Unitree’s business model is often quoted as direct evidence of this dynamic, and it is indeed true that hardware is the crux of Unitree’s success. But does that mean Unitree, and the Chinese robotics industry writ large, has less interest in generalizability or the intelligence frontier? The IPO disclosures indicate otherwise.

Unitree called on incoming investors to “realize humanity’s ultimate dream — AGI” 实现人类最终极的梦想—AGI with them. Their lawyer-drafted definition of AGI is “a form of intelligence that possesses general cognitive capabilities comparable to those of humans, capable of understanding, learning, and executing intellectual tasks across any domain, and autonomously reasoning, planning, making decisions, and continuously learning in unknown environments.”

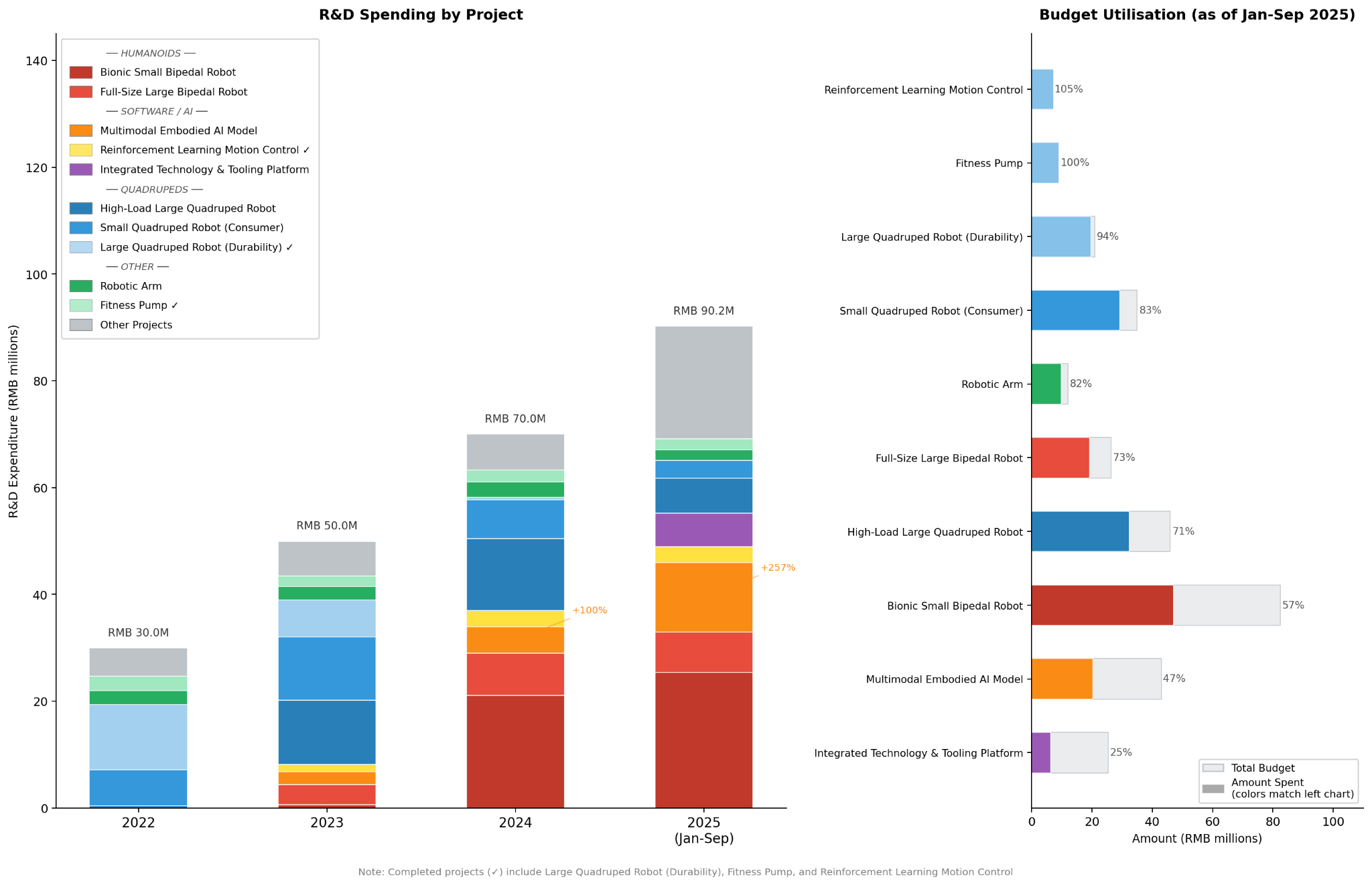

The financial reality tells us that most of Unitree’s R&D budget has gone to hardware. This is clearly downstream of their aforementioned focus on developing as many components in-house as possible to cut costs.

However, it’s important to notice in the chart above that Unitree’s R&D expenditure on “Multimodal Embodied AI Model” — the “big brain” of its robots — increased exponentially between 2024 and 2025, while other areas of R&D have grown at a steadier pace. Unitree is clearly ambitious about developing its models, even if it is known mostly for its hardware business.

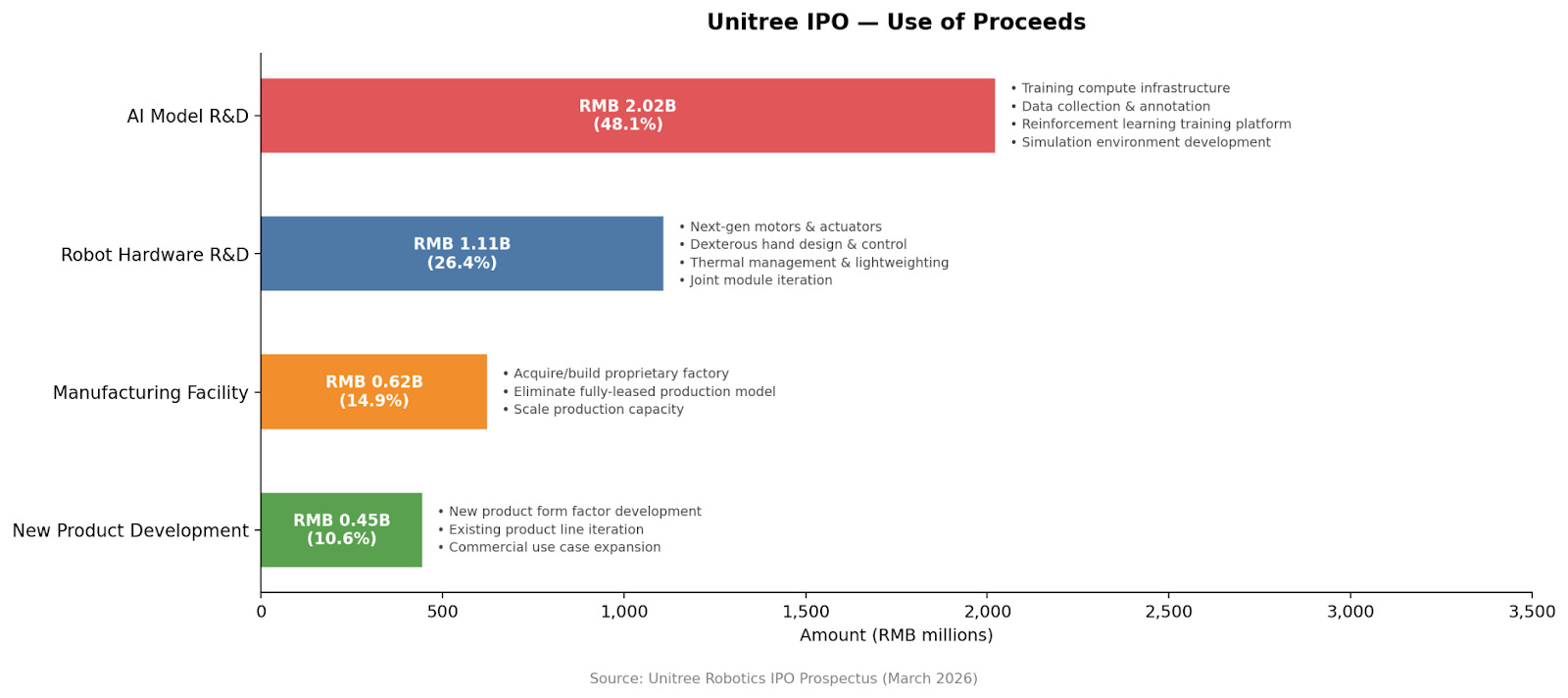

This becomes clearer when we look at Unitree’s plan for using the 4.2 billion RMB (around 607.7 million USD) raised through the IPO. Unitree’s stakeholders approved the following distribution in early 2026:

Nearly half of the IPO’s proceeds will be spent on training AI models over the next three years. That’s around 673 million RMB per year, which is not quite comparable to more well-known model makers (MiniMax, for example, spent around 1.75 billion RMB on R&D last year) but still a significant amount that signals long-term software ambitions.

Unitree currently owns no real estate, but plans to build its own factory with IPO proceeds. Per its disclosures, it has already secured a nod of approval from Hangzhou’s Binjiang District 滨江区 and plans to build there. Transitioning from an all-leased manufacturing model to proprietary manufacturing facilities is in line with their emphasis on in-house development and increasing production efficiency.

What comes next?

These disclosures answer many factual questions about Unitree’s business model, but raise more fundamental questions about the future of automation, US-China competitive dynamics, and both countries’ big bet on AI.

Question one: What will come of Unitree’s “AGI” ambitions? A public company is required to either use proceeds as stated in official disclosures, or publicly justify any changes. (Shareholders can vote to reappropriate funds, but unauthorized deviations could invoke China’s securities law and trigger scrutiny from the Stock Exchange.) Barring major issues, we should expect Unitree to spend handsomely on model training and development for the next three years. The biggest challenge will be making sure that these investments produce consequential returns. This uncertainty is not exclusive to Unitree; no one knows what the next three years will bring. But Unitree has now put itself on a path away from hardware-first and towards a more diversified strategy. This is, of course, risky, but relying on academia’s demand for hardware is no longer secure.

Question two: Will America turn against Unitree? A “Chinese military company” designation, which places companies into the annually-updated 1260H list, would merely exclude Unitree from contracting with the Department of Defense, but being placed on the Entity List would subject it to US export controls. Neither designation would prevent Unitree from selling to American customers outright, but they would hobble the company’s growth. As Unitree’s own prospectus describes:

Throughout the reporting period, revenue from overseas markets consistently exceeded 35% of total revenue. Should the United States continue to intensify trade and tariff policies that materially disadvantage Chinese exporters, or place the company on restricted lists governing procurement partnerships or technology export controls, the company faces the risk of being unable to sustain high growth in overseas sales — and potentially suffering an overall decline in performance. … Given uncertainty in industrial trade policy and the international political environment, any adverse shifts in external supply chain conditions or overseas market controls — compounded by further escalation of US trade restrictions and export control measures — could negatively affect the company’s ability to procure imported materials and maintain technology partnerships.

Policymakers eager to run “Trojan horse tech” out of America have to reckon with the dilemma that, for academic researchers at the forefront of embodied AI, there are few alternatives to Chinese-made hardware and platforms; Unitree is simply the most successful of the lot. Affordability and reliability are the most important factors for nonprofit academic labs. Robotics research is also a rough-and-tumble affair: there is wear and tear, and I’ve had researchers and students show me bruises they’ve sustained on the job from handling heavy humanoids. Unitree’s scale, consistency, and pricing meets academics where they are. Moreover, Unitree has been cultivating its relationships with international researchers long before the reporting periods of these IPO disclosures. The company started shipping internationally in 2018, and some of the earliest buyers of its quadrupeds were university research labs.

Imagine writing code for a dishwasher without dishwashers to test the code on. That’s a massively oversimplified comparison, but it is the same proposition in spirit. If Washington severs this symbiotic relationship, it will almost certainly make it harder for American researchers to maintain their lead in the software side of embodied AI.

Finally, question three: Can Unitree keep its lead inside China? As mentioned earlier, the company has formidable challengers in its own backyard, and has had to continuously trim costs to stay competitive. DEEP Robotics also joined the leagues of profitable companies in 2025. AgiBot’s CEO said at the end of last year that the company’s total sales revenue in 2025 likely exceeded 1 billion RMB. Up until now, Unitree’s success is arguably a case of first-mover advantage. Many more companies are taking up the Unitree playbook, and the future of robotics in China is far from determined.

If you aren’t yet ready to open your home to a robot dog, the company also sells fitness equipment inspired by robotics technology…